版权说明:本文档由用户提供并上传,收益归属内容提供方,若内容存在侵权,请进行举报或认领

文档简介

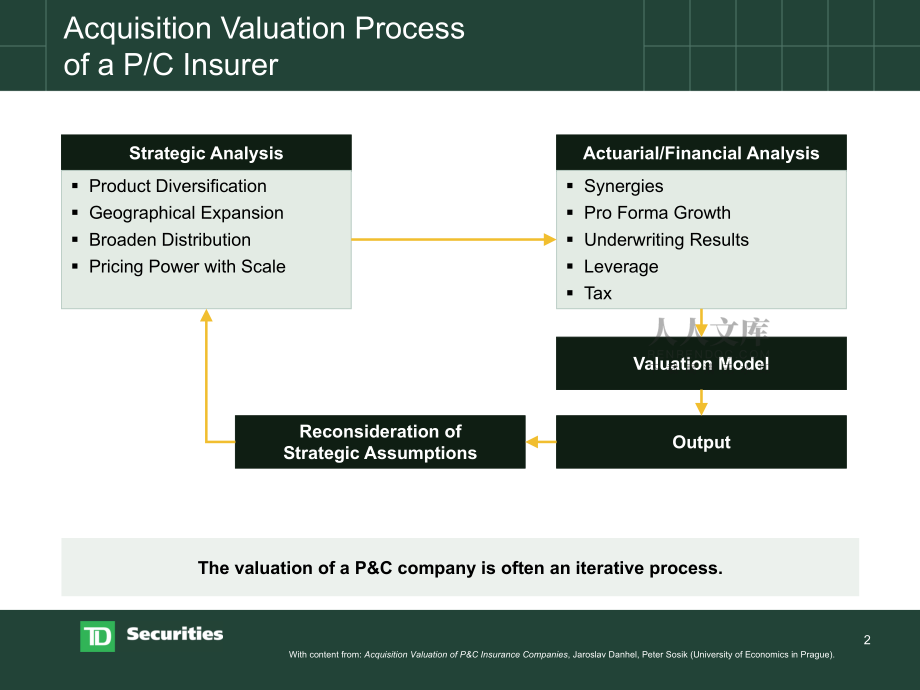

1、Valuation of a P&C CompanyPresented at CAS Spring MeetingJune 16, 2008 Quebec CitySean C. Martin, CFAVice PresidentFinancial Institutions GroupInvestment BankingTD Securities, Inc.2Acquisition Valuation Process of a P/C Insurer With content from: Acquisition Valuation of P&C Insurance Compan

2、ies, Jaroslav Danhel, Peter Sosik (University of Economics in Prague).Strategic AnalysisActuarial/Financial Analysis Product Diversification Geographical Expansion Broaden Distribution Pricing Power with Scale Synergies Pro Forma Growth Underwriting Results Leverage TaxValuation ModelOutputReconside

3、ration of Strategic AssumptionsThe valuation of a P&C company is often an iterative process.3Inputs to Valuation Process ActuarialCompany/Bankers/AccountantsPremium Growth by Business LineLoss & ALAE Ratios by Business LineULAEPayout PatternsExpensesReserve AdjustmentsInvestment YieldTaxCapi

4、tal Structure/Requirements4Valuation MethodsBook Value ApproachValue = value of assets value of liabilitiesAccounting focusedRetrospectiveFuture value of business not considered Stock Market ApproachValue = # of shares X share priceEfficient market hypothesisNo control premiumFuture value of busines

5、s may not be consideredDiscounted Cash Flow Approach (DCF)Value = Valuation of future profitSensitive to assumptionsValidate other methodsTt=1CFt(1-r)tWith content from: Acquisition Valuation of P&C Insurance Companies, Jaroslav Danhel, Peter Sosik (University of Economics in Prague).5Valuation

6、Methods (contd)Relative ValuationComparison to prices of:Precedent TransactionsPublic CompaniesPrice to Earnings (P/E) MultipleP/E = Price per ShareEarnings per ShareEarnings of Target Last-Twelve-Months (LTM) Forward (2008E) Normalized Post-SynergiesPrice-to-Book MultipleP/BV = Price per ShareBook

7、Value per ShareBook Value of Target Current Tangible (excludes Goodwill) Adjusted (reserve adjustments) 1.0 x value to excess capital6 Valuation “Football Field” - ExamplePreliminary Value Range (C$ per share)Comparable Companies plus Control Premium Precedent TransactionsComparable Companies Analys

8、t Target Prices (1)52 Week High - LowHistorical Average Trading Multiples (2)CanadaU.S. Implied Price / Book Value $221.5x$261.7x$302.0 x$181.2x$27.50$20.00$25.00$28.50$27.00$28.00$27.00Source: Bloomberg and Thomson.(1) Based on target prices from four of the seven companies covering XYZ.(2) Range i

9、s from average P/E to average P/BV from January 1, 2005 to January 1, 2007.$28.00$20.00Current Price: $20.00$24.00$23.00$23.00$24.00$25.007Comparable Companies - ExampleMarket Capitalization is on a diluted basis and includes in-the-money exercisable options outstanding.GAAP EPS is used for Canadian

10、 companies. Operating EPS is used for U.S companies and excludes tax realized gains and losses.Based on Bloomberg estimates.Multiples are calculated based on the closing price a day prior to the acquisition announcement by Liberty Mutual.8Precedent Transactions - ExampleSource: Bloomberg, SDC, MSA R

11、esearcher and various news servicesPrice/Earnings value calculated using 1H 2007 annualized net income.Price/Book value based on TD Newcrest estimate of adjusted book value.(1)1.4x transaction multiple estimated by TD Newcrest Analyst Doug Young and calculated as a percent of premiums, not book valu

12、e.United StatesCanada9 20% Premium, 16.0 x Price/Earnings, 1.6x Price/Book 50% Equity Consideration (132.5 shares delivered to existing shareholders of Sell Co.) $37 million after-tax cost of debt $30 million after-tax synergiesSimplified Acquisition Model - ExampleSource: Company reports and Bloomb

13、erg IBES estimates.Deal AssumptionsBuy Co.Sell Co.Share Price$10.00$20.00Shares Outstanding300100Market Capitalization$3,000$2,000Premium Paid20%Acquisition Price$2,400Acquisition Price per Share$24.002008 Earnings$300$150P/E (2008)10.0 x13.3xAcquisition P/E16.0 xBook Value$2,000$1,500P/Book1.5x1.3x

14、Acquisition P/BV1.6xSources and UsesSourcesCash$1757%Debt$1,15043%Equity$1,32550%Total Sources$2,650100%UsesPurchase of Equity$2,40091%Debt Refinanced$2008%Transaction Fees$502%Total Sources$2,650100%Other AssumptionsBuy Co. New Shares Issued132.5Cost of Debt5%Interest Cost of New Debt-$58After Tax

15、Cost of Debt-$37Synergies (after-tax)$30Total Adjust. to Net Income-$710 $1,150 of additional debt; 34% debt/capital ratio $1,325 new equity issued; equity of Sell Co. eliminated 2% EPS accretive after new shares issued, cost of debt and synergiesSimplified Acquisition Model Example Source: Company

16、reports and Bloomberg IBES estimates.Capital StructureBuy Co.Sell Co.AdjustPro FormaCash$75$100-$175$0Total Assets$5,400$3,700$0$9,100Debt$400$200$1,150$1,750Other Liabilities$3,000$2,000$0$5,000Equity$2,000$1,500-$175$3,325Total Assets & Liab.$5,400$3,700$10,075Debt/Capital17%12%34%EPS Accretio

17、n (2008)Buy Co.Sell Co.AdjustPro FormaEarnings$300$150-$7$443Shares Outstanding300132.5432.5Earnings per Share (EPS)$1.00$1.02Accretion/(Dilution)2%11 Sensitivity analysis highlights the impact on accretion of key deal assumptions Additional equity reduces accretion as additional shares are issued C

18、ost of equity is greater than the cost of debt Sell Co. acquired at a P/E ratio greater than Buy Co.Simplified Acquisition Model - ExampleSource: Company reports and Bloomberg IBES estimates.Sensitivity Analysis (2008 Earnings Accretion)2%0%10%20%30%$02%-2%-5%-7%$155%2%-1%-4%$309%6%2%-1%$4513%9%6%3%

19、2%0% 20%30%70%1%-2%-5%-8%60%5%2%-2%-5%50%9%6%2%-1%40%13%10%7%4%Purchase Price PremiumPurchase Price PremiumSynergiesEquity Consideration12 Excess capital of Buyer and Seller can be used to fund transaction The optimally capitalized portion of the Sell Co. business is valued at a full acquisition mul

20、tiple Excess Capital may not be valued at a full price/book multipleSimplified Acquisition Model - ExampleSource: Company reports and Bloomberg IBES estimates.Pro Forma Regulatory CapitalBuy Co.Sell Co.AdjustPro FormaRequired Capital$1,100$800$0$1,900Available Capital$2,000$1,500-$175$3,325Capital R

21、atio182%188%175%Minimum Target Ratio175%175%175%Excess Capital$75$100$0Adjusted Book Value of Sell Co.Book ValueBook Value MultipleEquity ValueCapital at 175%$1,4001.60 x$2,240Excess Capital$1001.00 x$100Total$1,5001.56x$2,340Base Case$1,5001.60 x$2,40013 Actuaries are an integral part of a P&C valuation process by providing forecasts for loss ratios, payout patterns, reserve development, and premium growth The valuation of a P&C company is often an iterative process where th

温馨提示

- 1. 本站所有资源如无特殊说明,都需要本地电脑安装OFFICE2007和PDF阅读器。图纸软件为CAD,CAXA,PROE,UG,SolidWorks等.压缩文件请下载最新的WinRAR软件解压。

- 2. 本站的文档不包含任何第三方提供的附件图纸等,如果需要附件,请联系上传者。文件的所有权益归上传用户所有。

- 3. 本站RAR压缩包中若带图纸,网页内容里面会有图纸预览,若没有图纸预览就没有图纸。

- 4. 未经权益所有人同意不得将文件中的内容挪作商业或盈利用途。

- 5. 人人文库网仅提供信息存储空间,仅对用户上传内容的表现方式做保护处理,对用户上传分享的文档内容本身不做任何修改或编辑,并不能对任何下载内容负责。

- 6. 下载文件中如有侵权或不适当内容,请与我们联系,我们立即纠正。

- 7. 本站不保证下载资源的准确性、安全性和完整性, 同时也不承担用户因使用这些下载资源对自己和他人造成任何形式的伤害或损失。

最新文档

- 2025年黑龙江省鹤岗市中小学教师招聘笔试试题及答案详解

- 2025年安徽省黄山市中小学教师招聘考试试题及答案详解

- 2026年阜新市清河门区街道办人员招聘笔试模拟试题及答案详解

- 2026年天津市西青区中小学教师招聘笔试参考试题及答案详解

- 2025年四平市铁东区街道办人员招聘考试试题及答案详解

- 2026年北京市顺义区街道办人员招聘笔试参考试题及答案详解

- 2026年咸阳市渭城区中小学教师招聘笔试参考试题及答案详解

- 2026年日照市岚山区中小学教师招聘笔试参考试题及答案详解

- 2026年朝阳市龙城区中小学教师招聘笔试参考试题及答案详解

- 2026年上海市长宁区街道办人员招聘考试参考试题及答案详解

- 象棋特级大师讲布局(定式与战理)

- 2026年中央一号文件解读:农村人居环境整治提升

- 和美乡村实施方案

- 医美安全生产管理制度

- 风机高处作业安全培训课件

- 用印流程规范制度

- 单位工会内控制度

- DB21-T 706-2025 森林经营技术规程

- 艺术培训机构教师聘用合同范本

- 2025年教师招聘考试教育综合基础知识备考全书

- 雨雾天气应急预案

评论

0/150

提交评论